Hargreaves Lansdown vs Legal & General - which is cheaper?

I invest in unit trusts through two brokers: Legal & General and Hargreaves Lansdown. But which is better? From a cost perspective, Hargreaves Lansdown is the winner. That's because Hargreaves Lansdown offers the same unit trusts for a cheaper price. Here's a comparison between Legal and General and Hargreaves Lansdown for some popular unit trusts:

| Fund name | Annual charge through Legal and General | Annual charge through Hargreaves Lansdown* |

|---|---|---|

| Pacific Index | 0.86% | 0.64% |

| UK 100 Index | 0.82% | 0.51% |

| Global 100 Index | 1.15% | 0.59% |

| Global Emerging Markets Index | 0.97% | 0.78% |

| Global Health and Pharmaceuticals Index | 1.15% | 0.76% |

| Growth trust | 1.82% | 1.38% |

| US Index | 0.82% | 0.51% |

| International Index | 0.89% | 0.53% |

Source: Legal and General and Hargreaves Lansdown

*Includes a 0.45% account maintenance fee

Why is Legal and General more expensive? It's because they only sell expensive R class funds. 'R' stands for 'Retail' because these funds are available to the general public, and because of this they are expensive. In contrast, 'I' stands for 'Institutional' and is cheap because it's usually only available to large corporate investors who buy in bulk. And I think 'C' class is a type of 'I' class, but I'm not sure.

Legal and General sent me an annual manager's report which provides more info:

{kind=link}

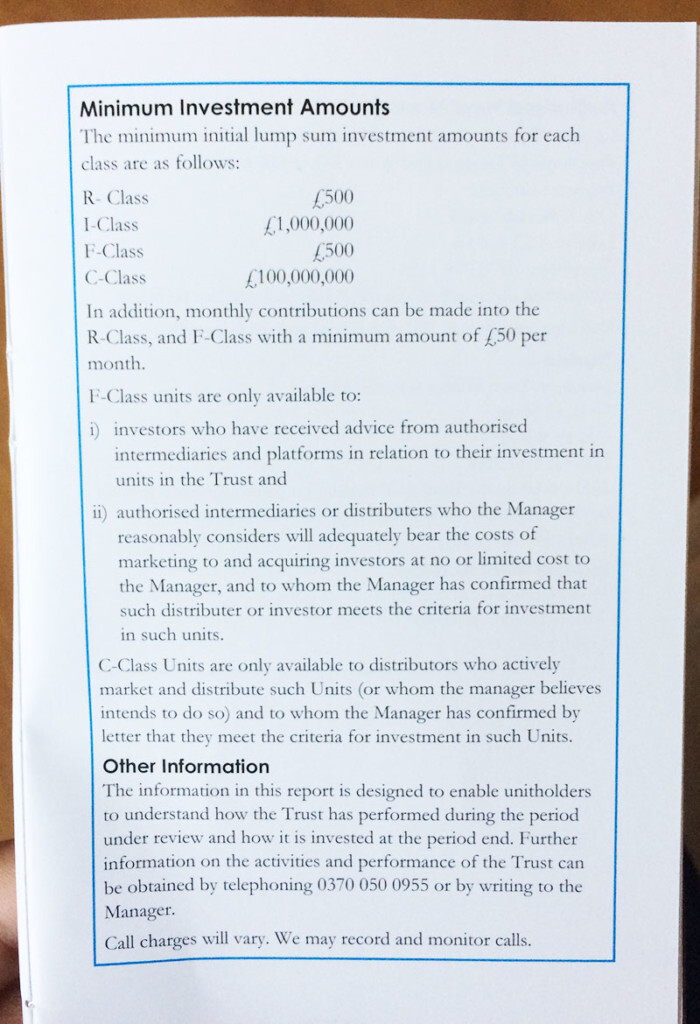

- C class units are only available to distributors who actively market and distribute the units. The minimum investment amount is £100 million.

- I class. The minimum investment amount is £1 million.

- R class. The minimum investment amount is £500.

So it seems the general public does have access to I class funds, but only if they have £1 million to invest. If you're not a millionaire, then you're stuck with the R class funds.

Hargreaves Landsdown, on the other hand, allows anyone to invest in I class funds, no matter how much you have to invest. As an example, take the Pacific Index fund. If you buy it through Legal and General, your only option is the R class version of the fund, which costs 0.86% per year. Legal and General do have an I class (which costs just 0.19% per year) and a C class (which costs just 0.14% per year!) but these aren't available to the average Joe. Hargreaves Lansdown, on the other hand, does let me buy the I class version for 0.19%. After I have added on Hargreaves Lansdown's management fee of 0.45% per year, the total fee is 0.65%, which is cheaper than Legal and General.

I asked Hargreaves Lansdown if there any other fees I should know about. This is what they said:

Each fund will have its own ongoing charge (OCF/TER), this includes the fund manager’s charge for managing the fund and any other expenses associated with the fund such as the fees paid to the fund’s auditors and registrars. This charge is deducted at source from either the income or capital of the fund.

There is a separate charging structure in place for funds held within Vantage, and this charge is applied across each Vantage account separately with no cap. For the first £250,000 of funds within each Vantage account, the charge will be 0.45% per annum. On the value of funds between £250,000 and £1m this will be 0.25% p.a. between £1m and £2m this will be 0.1% and there will be no charge on the value of funds above £2m.

There is no charge to sell your fund holdings, however, if you decide to transfer to another provider then you will be charged £25 per line of stock and an account closure charge of £25+VAT.

So basically, the charges are:

- The ongoing charge for each fund

- The annual Vantage account charge of 0.45% (that's if you have a Vantage account and your funds are less than £250,000, like mine)

- A transfer-out fee of £25 per line of stock (there's no fee if you transfer the funds yourself though - but if you let Hargreaves Lansdown do it for you, your funds will keep their ISA status)

- An account closure fee of £25 (but according to this article, you would only ever need to close your account if you're transferring all your ISAs to another provider)

Right now I have 71% of my investments in Legal and General and the other 29% with Hargreaves Lansdown. Given that Hargreaves Lansdown is cheaper, surely it would make sense to move my money from Legal and General over to them? So that's I'm going to do.

Comments

2020-10-20 David Lynch

It has just been announced that Fidelity UK have acquired Cavendish online, so it remains to be seen if Fidelity increase their platform fees. Fidelity have initially agreed to keep fees the same 'for at least twelve months'. On the face of it, it would seem that the Fidelity platform is a cheaper option for buying 'I' Class Legal & General units, but it's possible that the 'platform fee + Fund Management fee' may only be slightly cheaper than buying 'R' Class units directly from L & G.

Reply

2016-12-02 Dave Watson

I did the same thing a while back. But the 0.45% fee seems huge. Aren't there fixed fee online stock brokers who can manage these funds even cheaper?

Reply

2016-12-04 Paul Chris Jones

There are. I just haven't done the research yet. Keep in mind though that a relative fee broker can be cheaper than a fixed fee broker. It all depends on the size of the fixed fee and how much you have to invest. As an example: £10,000 investment with a £500 fixed fee = £9,500 left. £10,000 investment with a 1% relative fee = £9,900 left. Relative fee broker wins. £100,000 investment with a £500 fixed fee = £99,500 left. £100,000 investment with a 1% relative fee = £99,000 left. Fixed fee broker wins.

Reply

2020-02-25 neenthewiser

Glad I found this article. Had no idea L&G only offered R class units to it's own small investors. I notice the article is 4 years old. Has anything changed?

Reply

Leave a comment